Father’s Day Financial Security for Military Veterans Who Lost Primary Income

Understanding the Financial Challenges Military Fathers Face

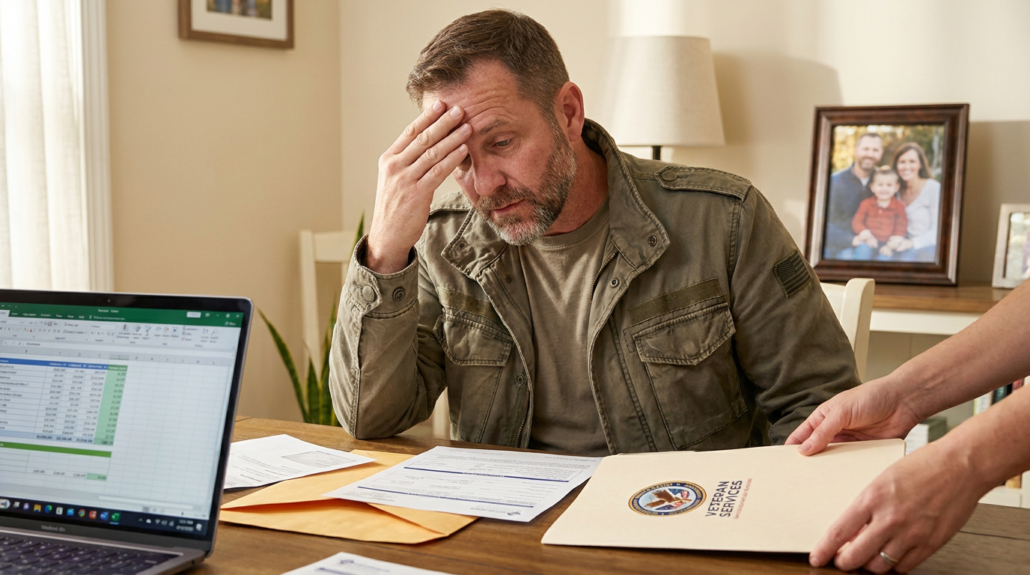

Military fathers transitioning from active duty face a perfect storm of financial challenges that civilian families rarely encounter. The steady paycheck, comprehensive benefits, and structured support system of military life can disappear overnight, leaving families scrambling to maintain their standard of living while navigating an unfamiliar civilian economy.

For many veteran fathers, the financial security they worked years to build can unravel quickly when faced with employment gaps, benefit delays, or unexpected medical expenses. These challenges become even more acute around significant dates like Father’s Day, when the pressure to provide for family celebrations compounds existing financial stress.

Transition-Related Income Loss and Its Impact on Families

The transition from military to civilian employment often involves significant income disruption that catches many families off guard. Veterans frequently experience employment gaps of three to six months while navigating job searches, credential transfers, and skill translations that civilian employers can understand.

Military compensation packages include housing allowances, medical coverage, and family support services that don’t translate directly to civilian paychecks. A service member earning $60,000 in total military compensation might need a $75,000 civilian salary to maintain the same standard of living once housing, healthcare, and other benefits are factored in.

Geographic relocation adds another layer of complexity. Families moving from areas with lower costs of living near military installations often find themselves in expensive civilian job markets where their military savings don’t stretch as far. This geographic adjustment can delay employment while families search for both suitable work and affordable housing.

The psychological impact of income loss affects the entire family unit. Children who grew up in stable military communities suddenly face uncertainty about their father’s ability to provide, while spouses may need to enter the workforce or increase their hours to compensate for reduced household income.

Common Financial Obstacles Veterans Encounter After Service

Veteran fathers face unique financial barriers that civilian job seekers rarely encounter. Security clearances, specialized military training, and leadership experience don’t always translate clearly to civilian hiring managers, creating employment gaps that strain family budgets.

Medical issues related to service often create unexpected expenses and employment limitations. A veteran dealing with PTSD or physical injuries may require ongoing treatment while also facing restrictions on the types of work they can perform. These medical considerations can limit earning potential just when families need financial stability most.

Credit challenges frequently emerge during transition periods. Military families accustomed to stable housing and regular income might find their credit affected by relocation costs, temporary unemployment, or medical bills not fully covered by VA benefits.

Educational benefits through the GI Bill provide valuable opportunities, but they also mean reduced immediate income while veterans pursue training or degrees. Families must balance long-term career benefits against short-term financial needs, often requiring financial stability support during education periods.

The Hidden Costs of Reintegration and Adjustment

Beyond obvious expenses like job search costs and relocation fees, veteran families encounter hidden financial drains during reintegration. Professional clothing for civilian interviews, certification fees for industry credentials, and networking event costs can quickly add up for families already managing tight budgets.

Mental health support often requires out-of-pocket expenses while waiting for VA services or when seeking specialized care not covered by veteran benefits. Family counseling, child therapy, and spouse support services become necessary investments in family stability but create additional financial pressure.

Technology and equipment needs for civilian employment can catch families unprepared. Home office setups, professional software, or industry-specific tools represent unexpected expenses for veterans transitioning to civilian careers requiring different technological skills.

Transportation costs increase significantly when veterans move from military installations with comprehensive services to civilian communities requiring personal vehicles for commuting, shopping, and accessing services previously provided on base.

How Family Responsibilities Compound Financial Stress

Military fathers often serve as the primary breadwinners while spouses manage frequent relocations and maintain family stability during deployments. When income becomes uncertain, the pressure to maintain this provider role intensifies emotional and financial stress.

Children’s needs don’t pause during parental job transitions. School expenses, extracurricular activities, and social pressures continue while fathers navigate employment uncertainty. The desire to maintain normalcy for children often leads families to delay addressing financial stability concerns until problems become critical.

Spouse employment challenges add complexity to family financial planning. Military spouses often face career gaps due to frequent moves and deployment schedules, making it difficult for them to quickly increase household income when needed.

Extended family support systems may be geographically distant, leaving veteran families without the informal financial safety nets that civilian families often rely on during difficult transitions. This isolation increases the importance of formal support programs and community resources.

Emergency Financial Resources Available to Veteran Families

Federal Benefits and Emergency Assistance Programs

Military fathers facing sudden income loss have access to several federal programs designed specifically for veterans in crisis situations. The VA’s Financial Hardship program provides emergency assistance for housing, utilities, and basic necessities when families face immediate financial threats. This program typically processes applications within 48-72 hours, making it crucial for fathers who need rapid intervention.

The Supplemental Nutrition Assistance Program (SNAP) offers enhanced benefits for veteran families, with streamlined application processes that recognize military service. Veterans can often qualify for expedited SNAP benefits, receiving assistance within seven days rather than the standard 30-day processing period. Additionally, the Temporary Assistance for Needy Families (TANF) program provides cash assistance and job training specifically tailored to transitioning service members.

Social Security Disability Insurance becomes particularly relevant for veterans whose income loss stems from service-connected injuries or conditions. The VA’s expedited disability claims process for veterans experiencing financial hardship can accelerate benefit approval from months to weeks, providing crucial income replacement during the most vulnerable period.

VA Emergency Financial Support Options

The Department of Veterans Affairs offers multiple emergency financial lifelines beyond standard disability compensation. The VA’s Emergency Financial Assistance program provides grants up to $2,500 for veterans facing immediate eviction, utility disconnection, or other housing-related crises. These grants don’t require repayment and can be approved within 24 hours in extreme circumstances.

VA’s Specially Adapted Housing grants help disabled veterans modify their homes to accommodate service-connected disabilities, potentially reducing monthly housing costs significantly. The program covers up to $101,754 for home modifications or $20,387 for adaptations to family members’ homes where the veteran will reside.

For veterans pursuing education, the VA’s Student Veterans Emergency Relief Fund provides emergency financial assistance for basic needs like food, housing, and utilities while using GI Bill benefits. Understanding how financial stress affects during transitions helps fathers identify when these emergency resources become necessary for family stability.

State and Local Veteran Relief Programs

Every state maintains veteran assistance programs that complement federal benefits, often providing faster response times for emergency situations. State Veterans Affairs offices typically maintain emergency relief funds ranging from $500 to $5,000 for qualified applicants. These programs frequently have less stringent eligibility requirements than federal programs and can bridge the gap while federal benefits get processed.

Local county veteran service officers serve as invaluable resources, maintaining relationships with community organizations and emergency assistance programs. They often have access to discretionary funds for immediate needs and can expedite applications through multiple programs simultaneously. Many counties also offer property tax exemptions for disabled veterans, reducing monthly housing costs permanently.

Municipal utility assistance programs specifically target veteran families facing disconnection threats. These programs often provide both emergency payment assistance and ongoing reduced-rate services for qualifying veterans. Local housing authorities maintain veteran preference lists for emergency housing assistance, recognizing the unique challenges military families face during financial crises.

Non-Profit Organizations Offering Immediate Aid

National veteran service organizations provide rapid response financial assistance that often fills gaps in government programs. The American Legion’s Temporary Financial Assistance program provides grants up to $3,000 for basic needs, with approval processes that can take as little as 48 hours. The VFW’s Unmet Needs program offers similar assistance, focusing specifically on unexpected financial hardships that threaten family stability.

Faith-based organizations and community foundations maintain emergency assistance funds specifically designated for veteran families. These programs often have fewer administrative requirements and can provide immediate assistance while families navigate longer-term solutions. Local United Way chapters frequently coordinate veteran assistance programs across multiple agencies, streamlining the application process for families in crisis.

Operation Family Fund and similar organizations understand that timely financial assistance from becoming overwhelming family emergencies. These organizations often provide grants for expenses that government programs don’t cover, such as vehicle repairs needed for employment or medical expenses not covered by VA healthcare.

Military relief societies including Army Emergency Relief, Navy-Marine Corps Relief Society, and Air Force Aid Society offer interest-free loans and grants specifically for active duty, retired, and veteran families. These organizations understand military financial challenges intimately and can provide assistance within hours of application approval, making them crucial resources for fathers facing immediate income loss.

Building Long-Term Financial Stability After Service

Career Transition Strategies and Job Placement Services

Military fathers transitioning to civilian careers face unique challenges that extend beyond simply updating a resume. Your leadership experience, technical skills, and ability to perform under pressure translate directly to civilian roles, but the key lies in effectively communicating these strengths to employers who may not fully understand military experience.

The Department of Veterans Affairs VR&E program provides comprehensive career counseling and job placement assistance specifically designed for veterans. This isn’t just about finding any job; it’s about building a career path that leverages your military background while providing the financial stability your family needs. Veterans typically see 15-20% higher starting salaries when they utilize professional transition services compared to those who navigate the job market alone.

Corporate America increasingly recognizes the value military veterans bring to their organizations. Many Fortune 500 companies maintain dedicated veteran hiring programs, understanding that your ability to maintain consistent performance under challenging circumstances translates directly to business success. Companies like Amazon, Microsoft, and JPMorgan Chase actively recruit veterans for leadership positions.

Federal employment presents another strong option. Veterans preference in federal hiring isn’t just a token gesture; it represents real opportunity for career advancement and job security. Federal positions often provide competitive salaries, comprehensive benefits, and clear advancement pathways that can support long-term family financial goals.

Education Benefits and Skill Development Programs

Your GI Bill benefits represent more than just educational opportunity; they’re a pathway to financial transformation for your family. The Post-9/11 GI Bill provides up to 36 months of education benefits, covering tuition, housing allowances, and book stipends. For military fathers, this means you can pursue degree programs or professional certifications while maintaining income through the monthly housing allowance.

Trade schools and vocational programs often provide faster pathways to well-paying careers than traditional four-year degrees. Electricians, plumbers, and HVAC technicians earn median salaries of $56,000-$73,000 annually, with many earning significantly more through overtime and specialized work. These careers also offer job security and opportunities for self-employment.

Professional certification programs in fields like cybersecurity, project management, or logistics can leverage your military experience while opening doors to six-figure careers. Many veterans successfully transition into cybersecurity roles, where your security clearance and understanding of risk management provide significant advantages. The median cybersecurity salary exceeds $95,000 annually.

Online education platforms specifically designed for veterans offer flexible scheduling that accommodates family responsibilities. Programs like VET TEC provide funding for technology training beyond your GI Bill benefits, allowing you to stack credentials while building your career foundation.

Small Business Opportunities and Entrepreneurship Support

Veteran entrepreneurship isn’t just about following a dream; it’s about creating financial independence for your family. The Small Business Administration’s veteran programs provide access to capital, mentorship, and contracting opportunities specifically designed for veteran-owned businesses. Veterans are 45% more likely to be self-employed than non-veterans, often achieving higher income levels through business ownership.

The SCORE mentorship program connects veteran entrepreneurs with experienced business leaders who provide guidance through the challenging early stages of business development. This mentorship significantly increases your chances of business success while helping you avoid costly mistakes that could impact your family’s financial security.

Federal contracting set-asides reserve billions of dollars in government contracts specifically for veteran-owned small businesses. Your military background provides credibility and understanding of government operations that civilian competitors often lack. Many veterans successfully build businesses around their military expertise, particularly in areas like security services, logistics, and training.

Building Credit and Managing Debt After Military Service

Military service often means limited credit history, which can create challenges when applying for mortgages, business loans, or other financial products essential for family stability. Understanding how to build credit strategically while managing existing debt determines your family’s long-term financial health.

VA home loans represent one of the most valuable benefits for military families, requiring no down payment and offering competitive interest rates. However, qualifying for the best rates requires strong credit scores. Many veterans benefit from working with credit counselors who understand military financial situations and can develop personalized strategies for credit improvement.

Student loan debt from pre-military education or spouse’s education can burden veteran families. Public Service Loan Forgiveness programs may apply to certain military service, and understanding how timely assistance can prevent small financial setbacks from derailing long-term goals becomes crucial for family financial planning.

Financial counseling services through Military Family Life Counselors help veterans develop budgeting strategies that account for irregular civilian income patterns while building emergency funds that provide family security during career transitions.

Protecting Your Family’s Financial Future

Life Insurance Options and Coverage Considerations

Military families often underestimate the importance of comprehensive life insurance coverage until they face a sudden income loss. Veterans who served in combat zones or experienced service-related injuries should prioritize reviewing their current coverage and exploring additional options beyond basic military benefits.

Servicemembers’ Group Life Insurance (SGLI) provides a foundation, but many veterans don’t realize they can convert this coverage to Veterans’ Group Life Insurance (VGLI) within 240 days of separation. The conversion window is critical because waiting too long means losing the ability to maintain coverage without medical underwriting. For fathers supporting families, this coverage becomes even more essential when considering the financial impact on dependents.

Term life insurance often provides the most affordable way to increase coverage amounts during periods of financial uncertainty. Veterans with service-connected disabilities may qualify for VA life insurance programs that offer coverage regardless of health conditions that might make traditional policies expensive or impossible to obtain. These specialized programs recognize the unique health challenges veterans face and provide accessible coverage options.

Consider the timing carefully. Many veterans delay purchasing additional coverage during financial hardship, but this approach can backfire if health conditions develop that make future coverage unattainable. Even modest increases in coverage can provide crucial protection for families already struggling with reduced income.

Creating Emergency Funds on a Limited Budget

Building an emergency fund while managing reduced income requires strategic thinking rather than perfect execution. Military families often approach this challenge with an all-or-nothing mindset, but successful emergency funds start with consistent small contributions rather than large lump sums.

Veterans should target an initial goal of $500 to $1,000 before pursuing the traditional three-to-six-month expense recommendation. This smaller target feels achievable and provides immediate protection against minor emergencies that might otherwise require credit card debt or borrowing. Even $25 weekly contributions can reach this initial milestone within six months.

Automatic savings transfers work particularly well for military families accustomed to structured financial systems. Setting up automatic transfers for the day after benefits or employment income arrives ensures the money moves before other expenses consume available funds. Many veterans find success using separate savings accounts specifically designated for emergencies, making the money less accessible for non-emergency purchases.

Consider unexpected income sources for emergency fund contributions. Tax refunds, VA disability compensation adjustments, or one-time assistance from organizations that provide financial support can jumpstart emergency savings when regular income remains tight. The key is treating these windfalls as opportunities to build financial security rather than addressing immediate wants.

Investment Strategies Tailored for Veterans

Veterans facing income uncertainty need investment approaches that prioritize stability and accessibility over aggressive growth. The Thrift Savings Plan (TSP) remains one of the most powerful tools available, particularly for veterans who can maintain contributions even at reduced levels during financial hardship.

Target-date funds within TSP accounts offer professional management and automatic rebalancing without requiring extensive investment knowledge. Veterans approaching retirement age should review their fund selections to ensure appropriate risk levels, while younger veterans can often maintain more aggressive allocations despite temporary income reductions.

Dollar-cost averaging works particularly well during periods of irregular income. Rather than trying to time investments perfectly, veterans can invest smaller amounts consistently when funds are available. This approach reduces the pressure to make large investment decisions during financially stressful periods.

Veterans should avoid completely stopping retirement contributions unless absolutely necessary. Even reducing contributions to minimal amounts maintains the habit and takes advantage of any available employer matching. Many veterans who completely stop contributions during hardship struggle to restart them once their financial situation improves.

Estate Planning and Beneficiary Designations

Military families often have complex beneficiary situations involving ex-spouses, children from multiple relationships, or family members who provided support during deployment periods. Regular review of beneficiary designations becomes crucial when income changes affect family dynamics and financial responsibilities.

Veterans should conduct annual reviews of all accounts including TSP, VA benefits, life insurance policies, and any employer-sponsored retirement accounts. Military service often creates unique family situations where traditional estate planning assumptions don’t apply, making professional guidance particularly valuable.

Basic wills and powers of attorney provide essential protection that many military families overlook until emergencies arise. Veterans can often access low-cost legal assistance through VA programs or veteran service organizations, making professional estate planning more affordable than many realize. For those needing immediate assistance with planning or other financial challenges, resources are available to help veterans access during difficult transitions.

Document storage and communication with family members about estate plans requires special attention for military families. Deployments, frequent moves, and service-related risks make it essential that beneficiaries understand how to access important documents and contact information when needed.

Support Networks and Community Resources

Connecting with Other Military Fathers Facing Similar Challenges

The isolation that comes with financial hardship hits military fathers particularly hard. You’ve served alongside brothers-in-arms who understood your mission, but civilian life can feel isolatingly different when you’re struggling to provide for your family. Finding other veteran fathers who’ve walked this path creates an immediate understanding that civilian support groups often can’t match.

Veterans of Foreign Wars (VW) and American Legion posts typically host informal gatherings where fathers share experiences beyond the official meeting agenda. These conversations happen over coffee before meetings start or during community service projects. The shared military experience creates instant credibility when discussing financial struggles, job search challenges, or the unique pressures of transitioning from military provider to civilian breadwinner.

Online communities through platforms like RallyPoint and Military.com offer 24/7 access to peer support. The anonymity allows for honest discussions about financial fears that might feel too vulnerable for face-to-face conversations. Many fathers find that typing out their concerns at 2 AM, when financial anxiety peaks, connects them with other veterans experiencing similar sleepless nights.

Family Support Services and Counseling Resources

Military Family Life Counselors (MFLCs) remain available to veterans through community-based programs, even after discharge. These counselors understand military family dynamics and the specific stressors that accompany financial instability. They provide practical coping strategies for managing family tension when money becomes the primary source of household stress.

VA Family Mental Health services extend beyond individual therapy to include family sessions focused on communication during financial crises. These sessions help military fathers articulate their concerns without creating additional family anxiety, while giving spouses and children tools to support the family’s financial recovery process.

Many installation Family Readiness Groups maintain connections with former members who’ve transitioned to civilian life. These networks often provide informal mentorship and practical advice from families who’ve successfully navigated similar financial challenges. The relationships built during active duty continue providing support through civilian struggles.

Financial counseling through Military Family Relief Societies addresses both immediate crisis management and long-term planning. These counselors understand military pay structures, benefits transitions, and the specific financial challenges that accompany leaving service. They provide guidance that’s tailored to veteran financial situations rather than generic civilian advice.

Mentorship Programs and Peer Support Networks

Team Red White & Blue chapters across the country connect veterans through athletic and social activities, but the relationships formed often extend into professional mentorship. Successful veteran entrepreneurs and business leaders within these chapters frequently mentor younger veterans struggling with financial stability, offering both emotional support and practical career guidance.

Corporate veteran mentorship programs through companies like JPMorgan Chase, Amazon, and Microsoft specifically connect military fathers with established veteran professionals. These relationships provide industry insights, networking opportunities, and often direct referrals to positions that offer family-supporting wages.

Iraq and Afghanistan Veterans of America (IAVA) operates peer-to-peer support networks where veterans at different life stages connect around specific challenges. Financial stability mentorship pairs recently separated veterans with those who’ve achieved economic stability, creating goal-oriented relationships focused on practical outcomes.

Local entrepreneur veteran groups often welcome struggling members seeking guidance on starting small businesses or developing income streams. The military leadership skills translate well to business ownership, and fellow veterans provide honest feedback about viable business ideas and potential pitfalls to avoid.

Local Community Organizations and Faith-Based Assistance

Churches, mosques, synagogues, and temples often maintain veteran assistance funds that operate quietly within their communities. Religious leaders understand the dignity concerns that accompany asking for help and structure assistance programs to preserve self-respect while providing necessary support.

Rotary Clubs, Lions Clubs, and similar civic organizations frequently sponsor local veteran families during financial crises. These groups appreciate military service and often provide assistance without extensive bureaucratic processes. Local business leaders within these organizations also serve as informal job placement networks.

Community foundations maintain emergency assistance funds specifically designated for veteran families. Local United Way chapters coordinate with multiple service providers to ensure comprehensive support that addresses both immediate needs and underlying causes of financial instability.

Food banks and community pantries operated by organizations supporting wounded veteran charity initiatives understand military families’ unique needs. They often stock items that accommodate dietary restrictions related to service-connected health conditions and provide resources with dignity and respect for military service.

Taking Action This Father’s Day and Beyond

Immediate Steps to Assess Your Financial Situation

This Father’s Day, take an honest inventory of your family’s financial position. Start by listing all monthly income sources, including VA disability compensation, unemployment benefits, or any part-time earnings. Document every expense, from housing and utilities to groceries and medical costs. Many veteran fathers discover they’re spending 40-50% more than their reduced income can support.

Create a simple spreadsheet or use a basic budgeting app to track where money flows in and out. Focus on identifying which expenses are absolutely essential versus those that can be temporarily reduced. This isn’t about permanent lifestyle changes but rather understanding your current reality so you can make informed decisions about seeking assistance.

Calculate how long your current savings will last at your present spending rate. If that number is under 90 days, prioritize applying for emergency assistance programs immediately. Even if you have several months of cushion, starting the application process now prevents financial stress from escalating into crisis.

How to Apply for Available Benefits and Assistance

Begin with the VA’s financial hardship assistance programs, which process applications faster than many civilian programs. The VA Hardship Program can provide temporary financial relief while you navigate longer-term solutions. Submit your application with recent bank statements, proof of income loss, and documentation of your military service.

Contact your local Veterans Service Organization (VSO) for application assistance. These representatives understand the paperwork requirements and can help ensure your applications are complete. They also know which programs have shorter waiting periods and can guide you toward the most appropriate assistance for your specific situation.

Don’t overlook state and county veteran assistance programs. Many states offer emergency rental assistance, utility payment programs, and grocery assistance specifically for veteran families. These programs often have less stringent requirements than federal programs and can provide relief within weeks rather than months.

Apply for multiple programs simultaneously rather than waiting for one decision before starting another application. Each program serves different needs, and approval for one doesn’t typically disqualify you from others.

Creating a Family Financial Recovery Plan

Develop a realistic timeline for financial recovery that acknowledges both immediate needs and long-term goals. Your plan should include specific milestones: when you expect to receive assistance, when you anticipate finding new employment, and when you project returning to financial stability.

Involve your family in age-appropriate discussions about the recovery plan. Children need reassurance that their basic needs will be met, while older family members can contribute ideas for reducing expenses or generating additional income. This collaborative approach reduces anxiety and helps everyone feel invested in the family’s financial recovery.

Build flexibility into your plan. Job searches often take longer than expected, and benefit approvals can face delays. Create contingency options for each major milestone. If your job search extends beyond three months, what additional assistance will you seek? If your savings deplete faster than projected, which expenses can you eliminate?

Set weekly check-ins to review progress and adjust the plan as needed. Financial recovery rarely follows a straight line, and regular assessments help you stay proactive rather than reactive to changing circumstances.

Honoring Your Service While Securing Your Family’s Future

Seeking financial assistance isn’t a reflection of personal failure but rather a responsible response to challenging circumstances. Military service taught you to use available resources strategically, and accessing veteran assistance programs demonstrates the same tactical thinking you applied during your service.

Connect with other veteran fathers who’ve navigated similar financial challenges. These relationships provide both practical advice and emotional support during a stressful transition. Many veterans find that sharing experiences reduces the isolation that often accompanies financial hardship.

Remember that organizations like wounded veteran charity programs exist specifically because communities recognize the sacrifices military families make. Accepting assistance allows these organizations to fulfill their mission of supporting those who served our country.

This Father’s Day represents an opportunity to model resilience and problem-solving for your children. By taking decisive action to address financial challenges, you demonstrate the same leadership qualities that defined your military service. Your family’s financial security isn’t just about immediate survival but about creating stability that honors your service and protects your family’s future.

Take the first step today, whether that’s completing a benefit application, scheduling an appointment with a VSO, or simply having an honest conversation with your family about your situation. Your decisive action today sets the foundation for your family’s financial recovery tomorrow.

Leave a Reply

Want to join the discussion?Feel free to contribute!